A Step-by-Step Guide on How to Start Bookkeeping for Your Small Business

Starting bookkeeping for your small business might seem like a daunting task, but with the right approach, it can be a manageable and crucial aspect of managing your finances.

In this comprehensive guide, we’ll walk you through the essential steps to initiate bookkeeping for your small business, helping you maintain accurate financial records and make informed decisions.

Understand the Basics:

Before diving into bookkeeping, it’s essential to understand the basics. Familiarize yourself with fundamental accounting principles such as debits and credits, assets and liabilities, and income and expenses. This foundational knowledge will be crucial as you start recording your business transactions.

Choose the Right Accounting Software:

Invest time in researching and selecting the right accounting software for your business. There are numerous options available, ranging from user-friendly platforms for beginners to more advanced systems for seasoned entrepreneurs. Popular choices include QuickBooks, Xero, and FreshBooks.

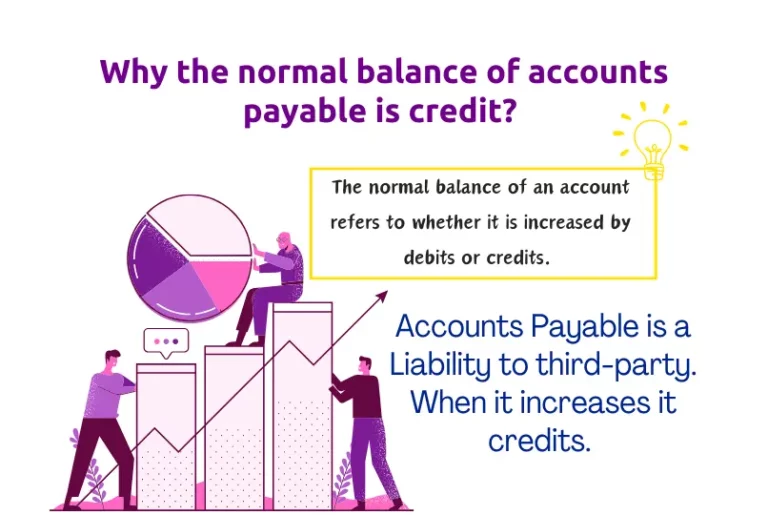

Set Up Your Chart of Accounts:

A chart of accounts is a categorized list of all your business accounts. It serves as the backbone of your bookkeeping system. Tailor it to suit your business needs, including accounts for assets, liabilities, equity, revenue, and expenses. Properly organizing your chart of accounts makes it easier to track and analyze your financial transactions.

Record All Transactions:

Be diligent about recording every business transaction. This includes sales, expenses, purchases, and any financial activities related to your business. Consistency is key, so establish a routine for entering transactions regularly. This habit ensures that you have an up-to-date and accurate financial snapshot of your business.

Reconcile Bank Statements:

Regularly reconcile your business bank statements with your accounting records. This process helps identify discrepancies and ensures that your financial records match your actual bank transactions. Reconciliation is a crucial step in maintaining the accuracy and integrity of your bookkeeping system.

Create a Filing System:

Develop a systematic filing system for your financial documents, such as receipts, invoices, and bank statements. This organization simplifies the retrieval of documents when needed and ensures that you have the necessary paperwork for tax purposes.

Monitor Cash Flow:

Keep a close eye on your business’s cash flow. Regularly review your income and expenses to understand how money moves in and out of your business. This insight is invaluable for making informed financial decisions and planning for the future.

Stay Compliant with Tax Regulations:

Familiarize yourself with local tax regulations and ensure that your bookkeeping practices align with them. This includes understanding deductible expenses, sales tax obligations, and any specific requirements for your industry. Compliance is essential to avoid penalties and legal issues.

Consider Professional Help:

As your business grows, you may find it beneficial to seek professional help. A certified accountant can provide expert advice, ensure compliance with tax laws, and offer insights to optimize your financial strategy.

Bottom Line:

Starting bookkeeping for your small business requires commitment and attention to detail, but the benefits far outweigh the initial challenges. With the right tools, knowledge, and a systematic approach, you can establish a robust bookkeeping system that empowers you to make informed financial decisions and drive the success of your business.